Spencer Williams

CEOSpencer Williams is CEO of Portability Services Network and Retirement Clearinghouse, a portability solutions provider.

Spencer Williams is CEO of Portability Services Network and Retirement Clearinghouse, a portability solutions provider.

When employees change jobs, auto portability can help avoid risky and premature cash outs.

The pandemic-driven migration out of big cities could lead to more missing participants, and going forward, more small, stranded retirement accounts.

Regardless of the political party that occupies the White House, bipartisan support for auto portability as a solution for helping more Americans, and especially minorities, increase their savings for retirement will remain strong.

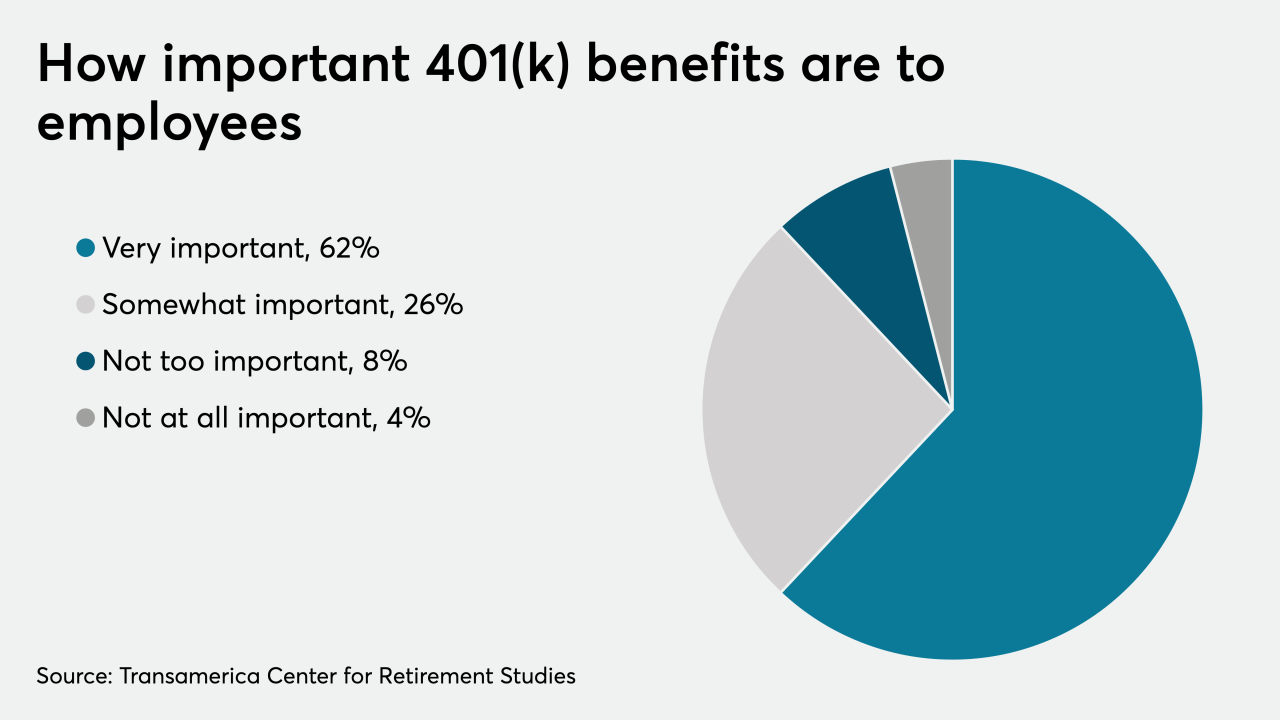

Just 23% of employees surveyed felt their employers were making a “significant effort” on financial wellness, and only 20% of employees expressed the same sentiment about retirement preparedness.

While we all hope for an end to the pandemic, and a return to economic and social normalcy, in 2021, interest rates are likely to stay at their near-zero levels for the foreseeable future. Every dollar will count for retirement-savers.

This year’s presidential election and COVID-19 have reminded us that many things are out of our control. But the power to help millions of Americans save more for retirement is in the hands of plan sponsors.

With rates likely to remain low, investors, and especially participants in sponsored 401(k) plans, need every dollar they can save to achieve their goals in retirement.

Defined contribution plan participants will seriously diminish their retirement savings if they prematurely cash out all or part of their 401(k) savings account balances.

Years from now, terminated employees may discover they have less income in retirement due to an automatic rollover or automatic cash-out from a previous employer.

The lack of seamless plan-to-plan asset portability prevents participants from easily moving and consolidating their 401(k) savings, leaving them open to the temptation to prematurely cash out their 401(k) accounts from prior employers’ plans.